Mr. Bean and I are lucky. We learned about savings and planning for retirement in our 20s and made sure to put it to good use.

Not everyone is so lucky. Over the last few years, some friends and relatives in the 50+ age range have mentioned that they have not even begun to think about saving for their retirement.

Considering a Federal Reserve report that came out in April 2021 stated that the Median Net Worth of Americans over 50 is only between $200,000-250,000, our family and friends are not alone. But it’s never too late to start your retirement planning.

The tips and steps in the post are aimed for those who are getting a late start but can obviously be used at any age to get your retirement savings going! The best time to start investing is yesterday, the second best time is NOW! 🙂

Step #1 Find Out Where You Are Now

Before you can make any financial decisions for your future, you need to know where you stand right now.

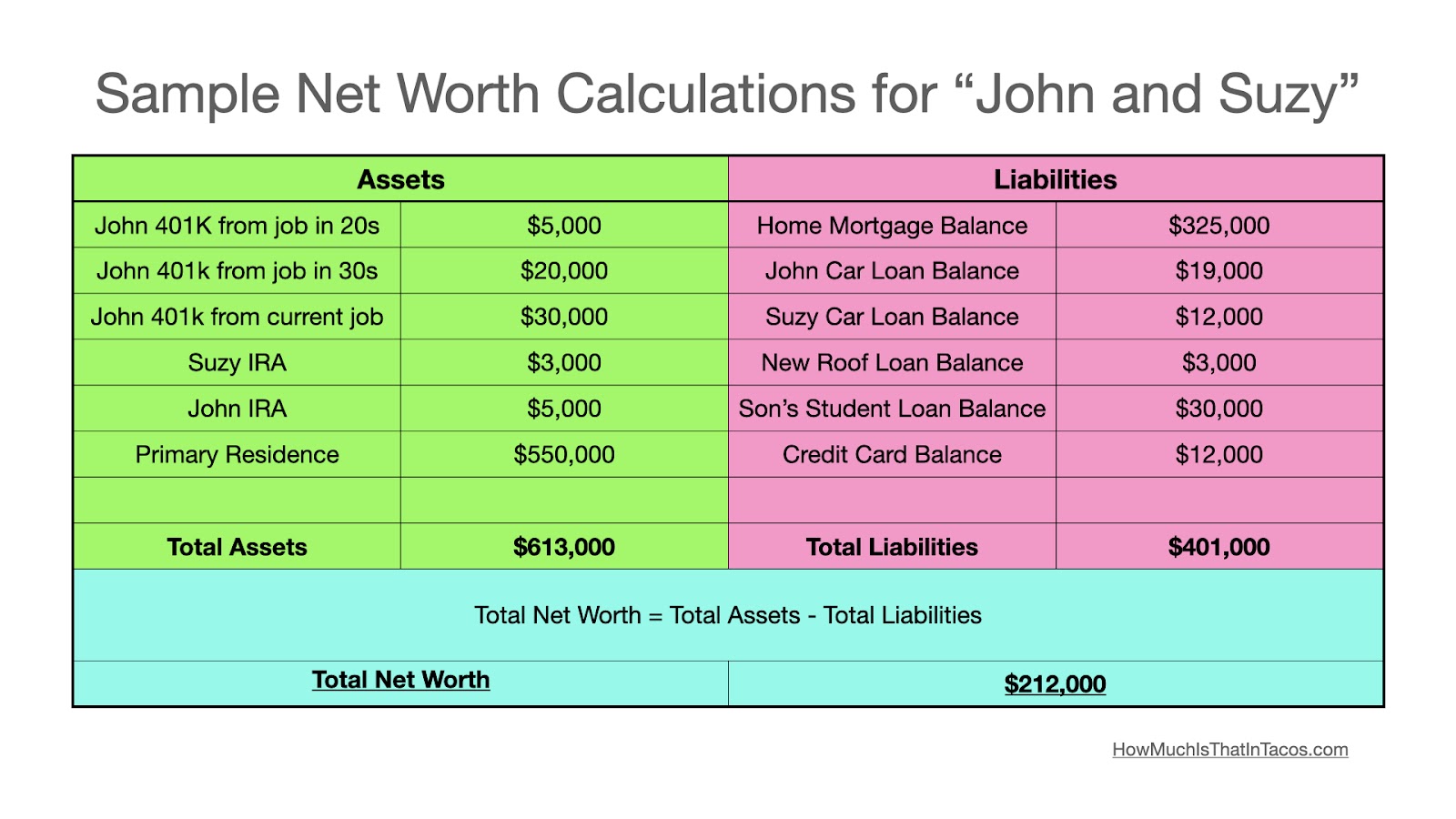

What’s Your Net Worth?

The first thing you need to do is find out your current net worth. To do this you need to go through all of your assets and liabilities.

An asset is something that brings money in. This could be a retirement fund or profitable rental property that pays you monthly rental checks. Your primary residence, the home you live in, is not technically an asset. You have to pay a mortgage if you still have one, insurance, and maintenance to keep it up. True, It will save you from having to pay rent in the future, if it is paid off, but it will always cost money thus it is technically a liability.

If you know it has appreciated and that you could potentially sell it in the future, you can consider it an asset, just make sure you balance the estimated value on the assets column with the remaining mortgage loan balance on the liabilities column.

A liability is anything that costs you money. This can be your car, your primary residence, or even your children as you have to feed, educate, insure, and generally pay for.

Do a quick summary to find out where you currently stand.

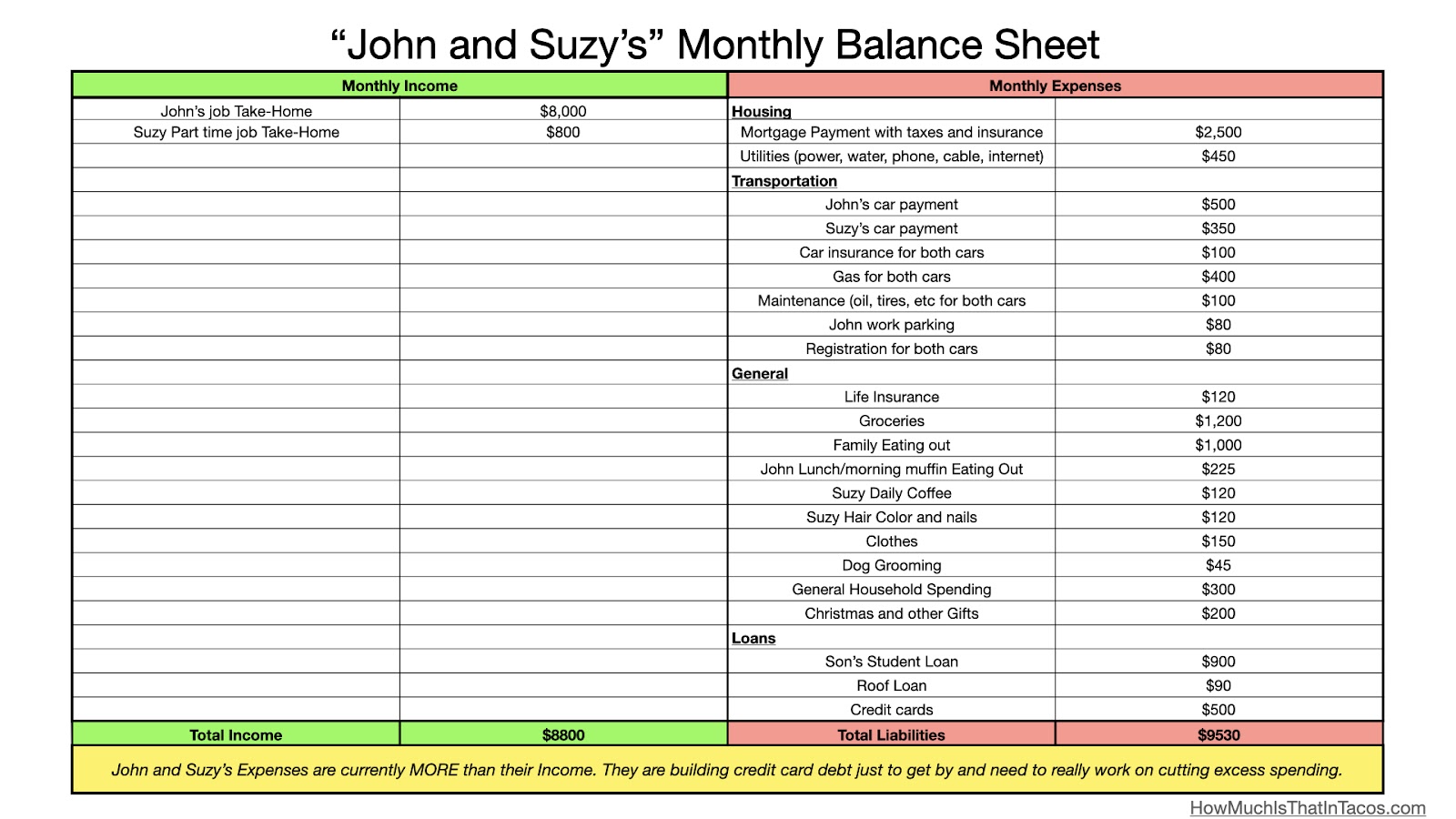

Income vs Expenses

The Second thing you need to figure out is your current annual/monthly income and expenses.

Your income is probably easy to figure out; it’s your paychecks plus any other places that money comes in from.

Your expenses may be a little bit harder to track down. This is where you need to pull out all of your bank statements and receipts to find out where your money is going.

If you do not use a single credit card or debit card for most of your purchases, you may have to track every penny in an app or by writing it down for a month or so to figure out where you are spending your money. Make sure you take every little thing into consideration: large payments like your mortgage or car payment, irregular payments like insurance or taxes, and all of the little things including coffee runs, new clothes, grocery trips, and credit card payments if you have them.

Once you know where you stand, you can move on to making any changes you need in order to build your retirement funds.

Where Are You Now?

- Find Your Net Worth = Total Assets – Total Liabilities

- Create Your Monthly Balance Sheet using Total Income – Total Spending

Step #2 Troubleshoot

Hopefully, after finding out where you are now, you realize that you have a good chunk of money that you can put away in your retirement account. But for most people, the reason you haven’t been putting away money in your retirement account is that you do not have a giant chunk of money sitting around at the end of every month. This could be caused by a couple of different things:

-Maybe your career has never really taken off due to jumping around from job to job thus never getting to a high-paying position or the opportunity to open a 401k or other employer-sponsored retirement plan.

-Maybe you had a life-threatening situation that caused a giant load of medical debt or some other issue that slowed down your savings and made you begin to feel helpless.

-Or for most people, maybe you were making a decent salary, but due to lifestyle inflation and keeping up with the Joneses, you have been spending your entire check, if not more, and have never made retirement savings a priority.

Figure out if what you really need is a decrease in expenses, an increase in income, or both. Once you know what you need to do, you can make those adjustments to get your savings going.

What Do You Need To Do?

- Is your income higher than your total spending? Start thinking about why, so you can do what you need to do to fix it.

Step #3 Make Necessary Changes

Now that you are getting closer to retirement age, you need to get serious and make some necessary changes to your lifestyle so that you will have enough money to enjoy a safe and comfortable retirement in the near future.

Cut Expenses

Take a moment and pretend in your mind that you have gotten rid of every single expense in your life. Wipe the slate completely clean of all liabilities and expectations. Then, slowly put back only the expenses that are necessary.

Start with Your Large Expenses:

- Maybe you currently have a $3,000 mortgage with a $500 a month electricity bill and a $150 a month HOA fee, is that actually necessary at this time in your life? If you love your home, it’s almost paid off, and think it will be the perfect place for you to grow old in, then maybe that is. But if you think you could get by with a smaller home, maybe a single story for easier aging in place, or living in a slightly less expensive neighborhood, you could bring that expense down to $2,000 a month or less.

- If you have a $700-a-month car payment, that is probably not absolutely necessary right now. (Like for anyone, ever.) Would you be able to sell your car and buy something just as usable, hopefully with even better gas mileage, paying cash, or at least bringing down your car payment to 5% or less of your income? (FYI, Car payments should never be more than 5% of your gross income and should never take more than 36 months to pay off, otherwise that legit means you can’t afford it.)

- Do you have adult children who are living with you, paying no rent but constantly going out and expecting you to provide them with food, shelter, and laundry services as if they were still 12? Helping your kids to get a leg up at the beginning of their careers is wonderful, but make sure they are also putting in the effort to take care of themselves and save for their own future. Show them how important it is and maybe walk through these steps with them together. The extra money that you are still spending on them every month when they are (hopefully) earning their own money but spending it all on Amazon and going out with their friends, could be put toward your own retirement funds.

Tackle Smaller Expenses

Once your larger expenses have been tweaked, you can start attacking the smaller expenses that tend to sneak up in life.

- Do you have a gym/newsletter/music app/whatever membership that you don’t use? Cancel it.

- Are you paying for 2,000 cable channels when you only watch the same three shows every week? Between Hulu and movie websites, there’s really no need to be paying more than $20 a month for any form of TV entertainment. (If your security in retirement is on the line, watching your favorite show a season late isn’t so bad.)

- Are you buying all of the newest books and just letting them sit on your bookshelf in your “to-be-read” pile? Hit up the library! Make the librarian your best friend and request books/movies/magazines you want. The library is awesome! If you haven’t been in years, go renew your library card tomorrow.

- Do you have a daily coffee addiction that requires you to stop by your favorite coffee shop multiple times a day? Limit yourself to a treat or two during the week but invest in a decent coffee machine and make your coffee at home on the regular.

When you’ve got all of your expenses as minimal as you possibly can, start putting it into action! Create a budget for yourself and your family. Obviously, if you have a spouse, you’re going to need to discuss this together so you’re on the same page. Show them the numbers so you can get excited about retirement together.

Start Living With Your New Budget

For the first month or so, this new budget may feel very restrictive. It might kinda suck but you will discover something: some things you are perfectly fine not having while others you’ll realize definitely need to be added back in.

People who go out to get their hair and nails done on a monthly basis, pick up coffee twice a day, and do a retail therapy session at Target every week, may cut all that out.

After a month or so, you may realize that you can do without your twice-daily coffee stop or Target therapy sessions but actually have better self-confidence if your hair looks nice. Add back getting your hair done once a month but leave out the other things.

(Or the other way around, maybe you don’t give two hoots what your hair looks like but that cinnamon brûlée just can’t be replicated at home so you get it once a week as a treat.)

If you’ve got all of your expenses cut and found places to adjust, hopefully, you will find a decent amount of money that you can now put toward your retirement. Yay! If you still do not feel that it is going to be enough, it might be time to look at increasing your income so that you can stock away as much as possible. A comfortable retirement is in your grasp, keep going!

Increase Income

When you are down to the line and want to be able to retire in the next 10 or so years but have nothing saved and can only cut your costs so much, you might need to get serious about bringing in extra income.

- If you’ve got some years of experience in an industry, you could work as a consultant on the side.

- Learn some new skills or even trade companies to get that promotion you’ve been after.

- Take on a part-time job delivering pizzas or working as a cashier at a grocery store.

- Or maybe you need to find something that you are really good at and could potentially start your own business or quickly advance in that new career, allowing for a larger salary.

Taking on extra work as you’re getting older may not sound like your idea of a good time, but it’s better to do it now, while you still can, than be stuck at Walmart in your 80s. YOU CAN DO THIS! This is just a temporary push so make the most of it and stockpile every extra dollar you bring in.

Make Necessary Changes

- Decrease Large Expenses in your life

- Housing

- Transportation

- Excess Dependents

- Decrease Smaller Expenses

- Unused Memberships

- Entertainment costs

- Shopping

- Excess “treats”

- Phone Plans

- Increase Income

- Part-Time job/ Start a part-time side business

- Promotion/bonuses

- Change Careers

Step #4 Pay Off Debt

Once you decrease your expenses and increase your income as needed, the next most important step is to make sure that all of your debts are paid off.

Get rid of your car payment. Try to get any mortgages paid off before you stop working. And definitely make sure that you have no credit card or other high-interest loans of any kind. Use your newfound money and create a debt snowball.

Pay off Debts Using a Debt Snowball

- Credit Cards

- Student/other Loans

- Car Payments

- Mortgage

Step #5 Fully Fund All Available Retirement Funds

Because of the wonders of compound interest, you want to have as many years for your money to grow as possible.

While you are paying off any debts you may have, ensure that you are getting any possible employer matches from employer-sponsored retirement funds like a 401k. If your employer matches your contributions up to a certain percentage, make sure you are at least putting in that amount. Once you have paid off all of your high-interest loans, like 5% APR or higher, try to fully fund all available retirement funds.

If you have access to a 401k, TSP, 403b, or other retirement plans from your employer, make sure you are putting in the maximum amount allowed in the tax code; for 2023, that is $22,500 for people under 50 or $30,000 for those over 50 due to the available $7,500 catch-up contributions. If you own your own business, you can open a SEP IRA or Solo 401K.

In addition to an employer-sponsored or self-employment account, you should also open an IRA (Individual Retirement Account) at a low-cost brokerage firm, like Vanguard or Fidelity. The 2023 limit is $6,500 for those under 50 years old and $7,500 for those over 50 due to the $1,000 catch-up allowance.

The nice thing about IRAs is that a non-working spouse can open one as well. If one spouse is the “sole breadwinner” of the household, the “stay-at-home” spouse can open and contribute money to their own IRA account as well, allowing a couple over 50 to put away $15,000 a year together! That’s a big help when you’re trying to put away as much money as possible in a tax-efficient way.

Fully Fund Your Retirement Accounts

- Max Out Employer Sponsored 401K, Etc

- Max Out IRA

- Ensure your spouse is maxing out their IRA as well, whether working or not

Once you have achieved all of this, you should be on your way to building up a solid retirement. Better late than never!

Just make sure you actually invest your retirement funds in stocks and bonds (age-based or total market index funds are the easiest, check out my article on Super Simple Investing). So many people kick themselves after doing all the work of opening an account and saving money, just to learn years later that they never actually invested it so it was just sitting in a money market account earning less than 1%. Make that money grow!

Wrap- Up

You may feel depressed thinking about all the work you need to do in order to get ready for retirement when it’s looming in the near future, but you can do this! Find out where you stand, make adjustments as needed, get rid of any debt, and invest, invest, invest! You got this!

Late Start Retirement Planning

- Find Out Where You Are Now

- Total Net Worth = Assets – Liabilities

- Create Your Monthly Balance Sheet use Total Income – Total Spending

- What Do You Need To Do?

- Is your income higher than your total spending? Start thinking about why.

- Make Necessary Changes

- Decrease Large Expenses in your life

- Housing?

- Transportation?

- Excess Dependents?

- Decrease Smaller Expenses

- Unused Memberships

- Entertainment costs

- Shopping

- Excess “treats”

- Phone Plans

- Increase Income

- Part-Time job/ Start a part-time side business?

- Promotion/bonuses

- Change Careers

- Decrease Large Expenses in your life

- Pay off Debts Using a Debt Snowball

- Credit Cards

- Student/other Loans

- Car Payments

- Mortgage

- Fully Fund Your Retirement Accounts

- Max Out Employer Sponsored 401K, Etc

- Max Out IRA

- Ensure your spouse is maxing out their IRA as well, whether working or not

Share this:

I’ve got some family members in the same position. I’ll definitely pass your article on to them.

It’s a very common thing. I hope the info can help them get started.:) Glad you enjoyed the article.